graph-model-1

Before we get to this month's big story, you really should meet graph-model-1, the most comprehensive, accurate, and expressive business data set.

Since 2023, we've been completely rebuilding our entity resolution framework, data processing engine, as well as the Enigma Console, where you can interact with this data and derive new insights.

Here, a “business” isn’t just a single branch or registration record; it’s the sum of everything we know: from its brand identity and legal frameworks to the physical footprints where it operates, the individuals who hold key roles or ownership stakes, and so much more.

With graph-model-1 you can:

It's all possible because of:

We're inviting partners to sign up for early access via the API and Console today by signing up for our Research Preview. We're eager for close collaborators and technical partners.

How Shopify outperforms its competition online

Shopify is the dominant online commerce platform, leading, outpacing competitors like Wix, Squarespace and Woocommerce.

Digging deeper using Enigma’s graph-model-1 data, a far more interesting theme emerges: dominant online sellers are choosing Shopify over its competitors.

Or at least, that seems to be the case.

For instance, here’s clothing stores that use Shopify vs those who don’t:

The premium looks roughly the same for candle stores that use Shopify (clearly, someone who is good at economy is helping candle shops):

If it seems that clothing and candle shops were chosen at random, don’t worry – they weren’t. They’re among a cohort of business types where the Shopify revenue premium – the difference in revenue between merchants using Shopify and those who aren’t – is among the highest.

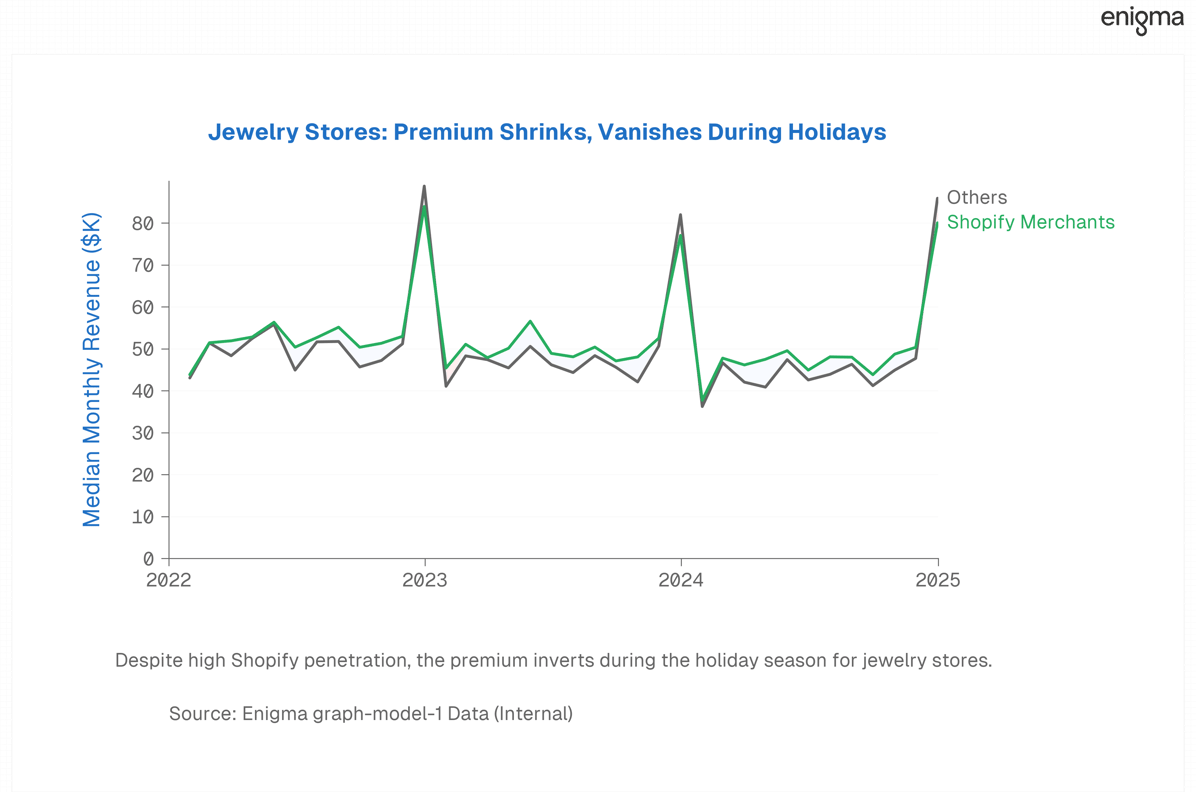

While this data alone doesn’t say anything about causation per se, you might assume that the Shopify premium exists in industries where Shopify has grabbed outsize market share. But that isn’t the case. Jewelry the a category with the highest Shopify penetration, but look at this chart: a very marginal revenue premium for the Shopify merchants across most of the year, and then none whatsoever during the winter holiday season, their biggest period of the year.

Zooming out helps piece together what’s going on.

Coffee shops, pizza places, shoe stores, restaurants, and vitamin and supplements shops consistently show the highest Shopify premium: industries characterized by numerous, small dollar value purchases, physical storefronts combined with online purchases, relatively simple inventories, and a fairly steady churn of failed businesses followed by new entrants.

What industries consistently show the worst Shopify premium? Furniture and wholesale. Industries characterized by large players with established manufacturing capabilities, extensive logistics operations, large per ticket value, a massive number of SKUs, and a comparatively low number of new entrants.

The Shopify premium shows that for Shopify, the customer acquisition process is a search for winners.

The merchants with the highest Shopify premium are in industries with extremely high failures rates. Over time, Shopify cannot succeed as a service provider in those industries by simply maintaining a steady customer base. It must find winners among new entrants. At scale, that means onboarding a lot of eventual losers and holding on to the few winners.

The Shopify premium exists in industries where that’s a viable strategy. It works well for that new coffee shop around the corner that just might make it, but less well for a decades-old supplier of industrial parts to commercial buyers.

(And somehow I made it through writing this whole section without once accidentally writing Spotify Premium.)

That's it for this month. Send any feedback, story tips, or up-and-coming Fintech Soundcloud Rapper cosigns to updates@enigma.com.