The State of Small Business Lending: June 2020 Industry Poll

Financial institutions that lend to small businesses have become “economic first responders”, as these institutions are working hard to resolve the extreme financial challenges presented by COVID-19. It’s no secret that many small businesses are in distress, and the destabilization they’re experiencing is sending shockwaves back to the institutions that serve them.

We decided to check in with the small business lending community to learn what’s happening on the ground at their institutions. What are these institutions experiencing right now, and what do they predict will happen in the next six months? Over the past week, Enigma polled 30 professionals across risk, credit, underwriting, and SMB business lines to get their takes on what’s happening in the world of small business lending. The poll results are summarized below.

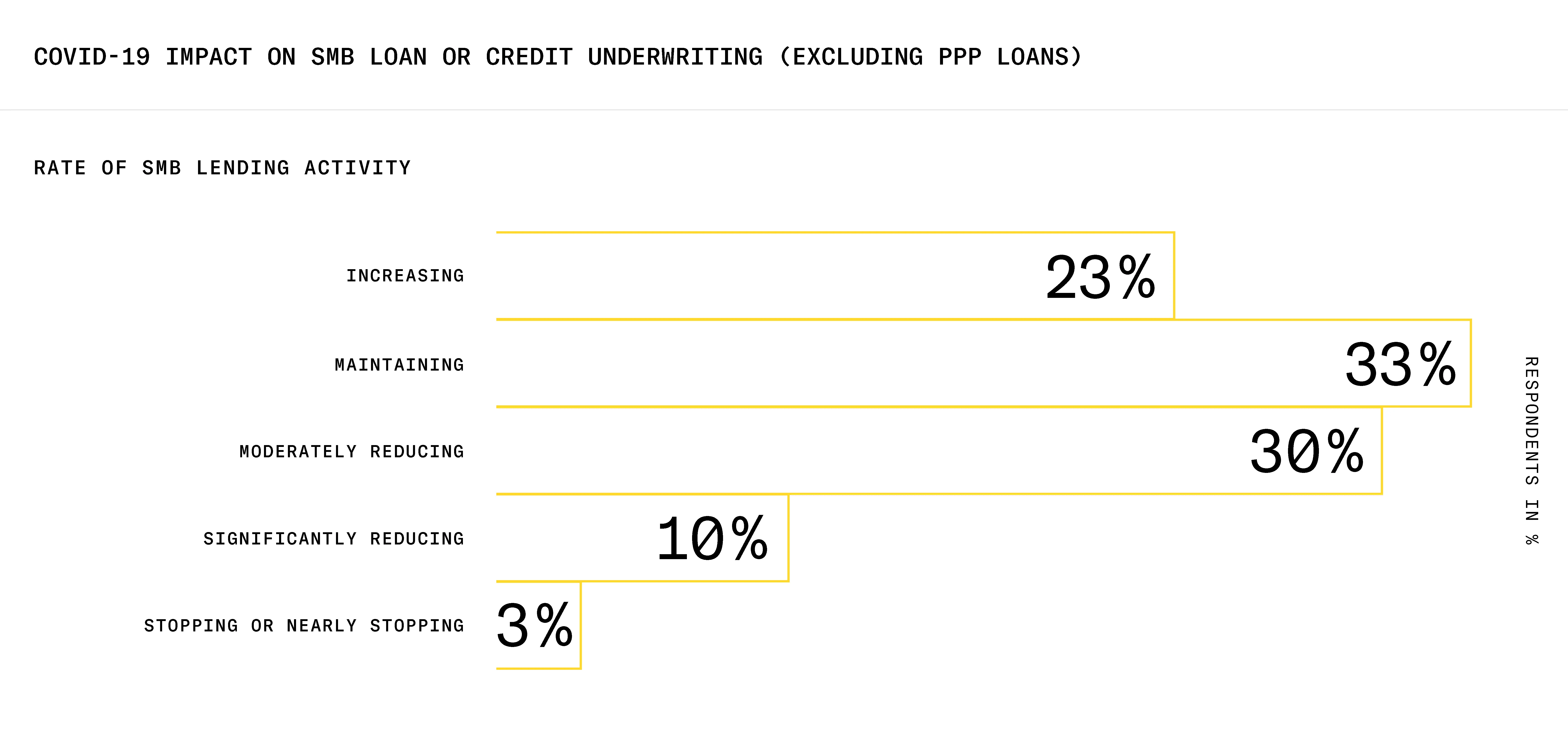

The impact of COVID-19 on SMB lending varies widely.

There was no singular dominant response when we asked participants about how COVID-19 affected their institution’s loan or credit underwriting for small businesses. The responses instead revealed that institutions are responding to COVID-19 differently and with varying degrees of intensity.

Perhaps most heartening was the fact that more than 50% of institutions are maintaining or increasing lending to small businesses, even exclusive of Paycheck Protection Program (PPP) loans. This signifies that many institutions are able to continue to provide small businesses access to credit and capital.

At the same time, more than 40% of participants noted that their institution was moderately or significantly reducing loan or credit offers to small businesses. Thus a good number of institutions are operating more conservatively right now to reduce risk exposure.

Constrained lending behavior may not last long. About ⅓ of participants believe their institution will return to pre-COVID levels of lending activity in six months. This positive outlook is further reinforced by the fact that few participants think their institution will limit or reduce their small business customer portfolio.

While lending activity may bounce back relatively quickly, 40% participants do believe credit or loan eligibility standards will become more stringent for small businesses in the future.

One participant stated, “The real issue is whether our credit standards will be somewhat tightened given current circumstances, by, for example, requiring lower LTV’s, higher minimum debt service coverage, more equity in development projects, and stronger personal guarantees from owners and sponsors.”

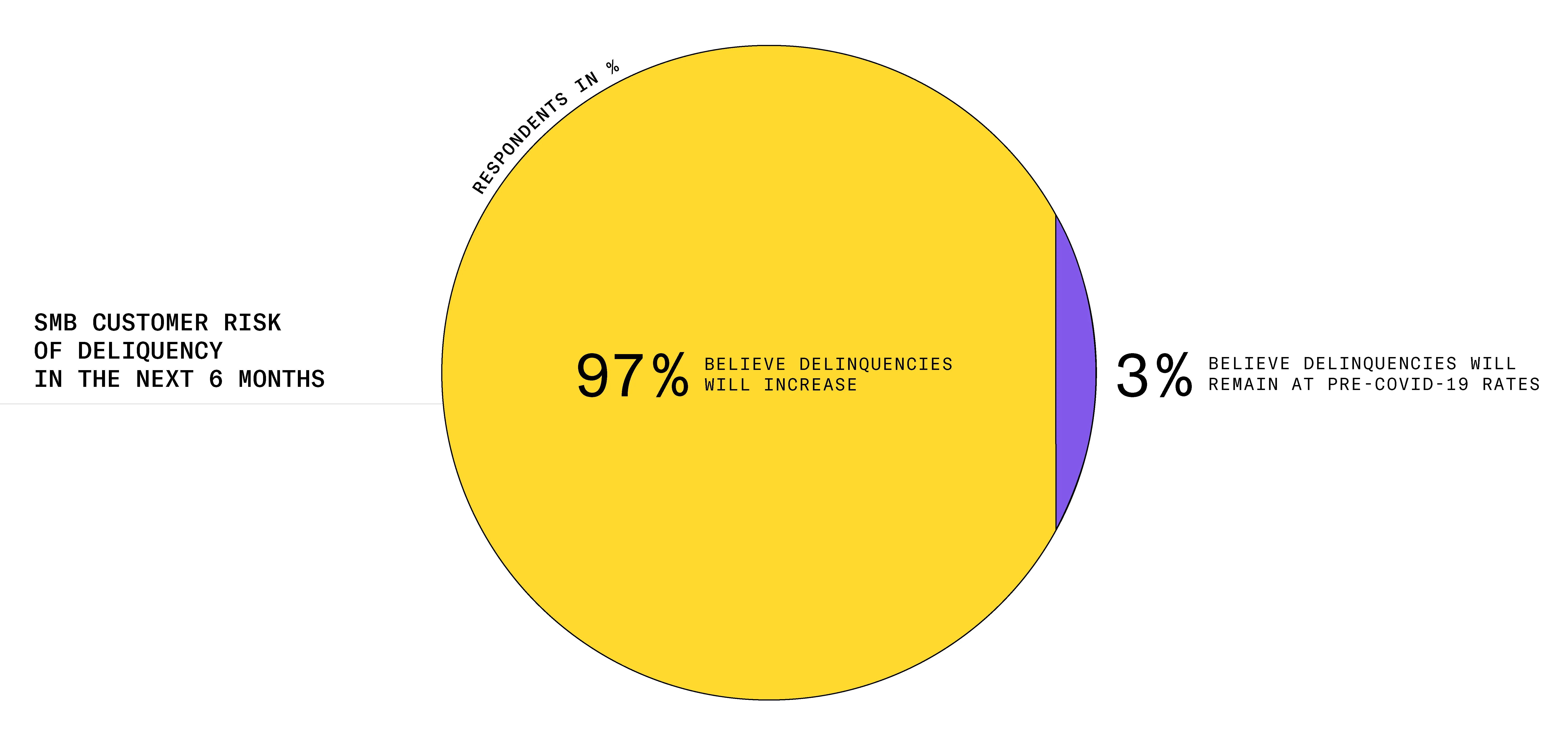

Everyone agrees delinquencies will rise.

97% of participants believe small business customer delinquencies will increase. This overwhelming response is unsurprising given the widely-known statistics about small business distress. Our participants are likely watching this data play out in real time amongst their institutions’s small business customer base.

However, the majority of participants (70%) believe delinquencies will only moderately increase, as compared to 27% that said delinquencies will increase significantly. This could reflect that institutions believe small businesses are poised to recover, perhaps thanks to government interventions such as the Paycheck Protection Program.

Note that only 23% of participants believed their institution would incur significant losses due to small business distress or delinquency. We attribute this either to the respondent institutions not being over-leveraged across their small business portfolios, or perhaps feeling that these delinquencies may be resolved as soon as small businesses are able to start operating more normally.

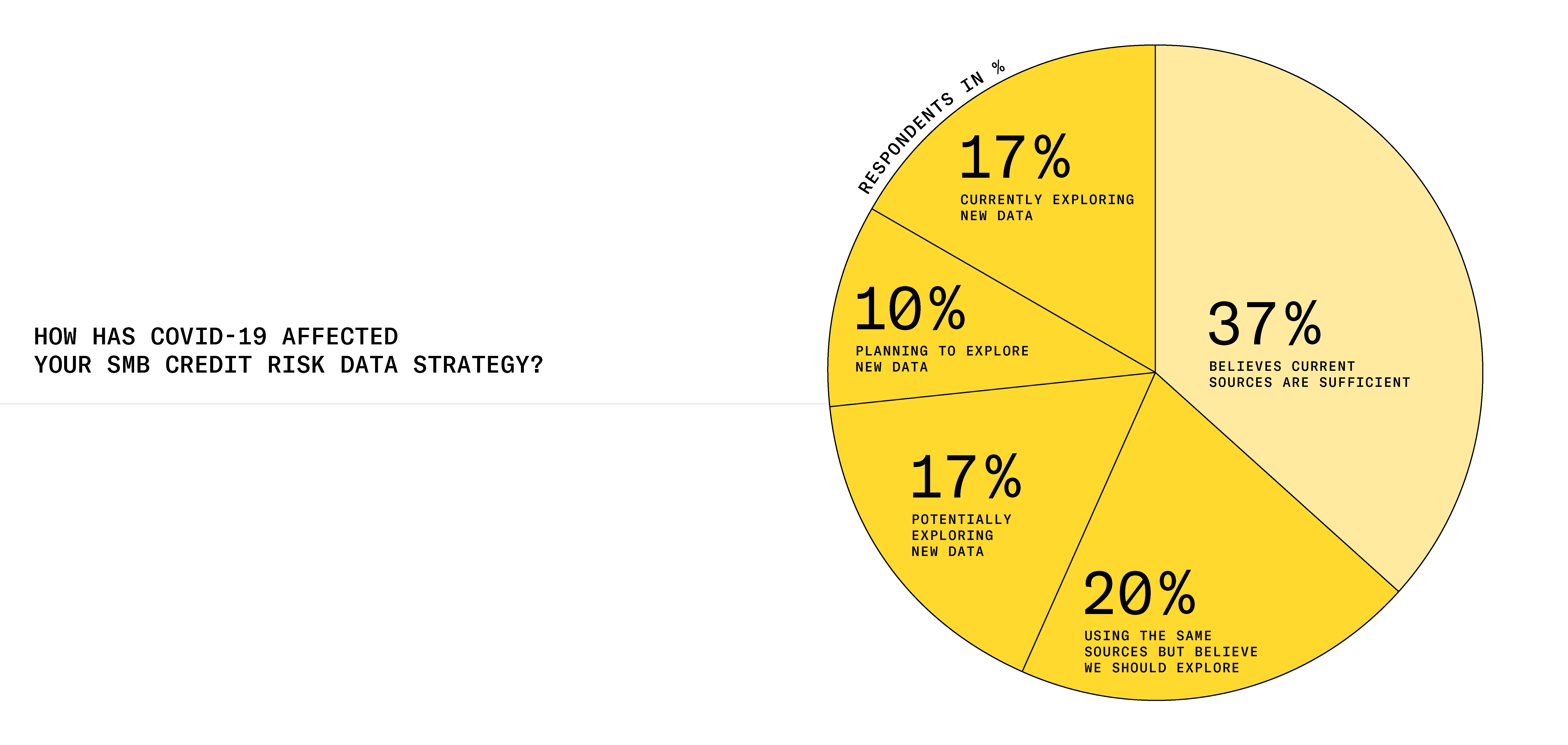

1 in 3 institutions is interested in new data sources for small business credit risk.

When asked about looking into new data sources for small business credit risk, more than 25% of participants said their institutions were currently exploring or planned to explore new sources of credit risk data. Another 20% of respondents said their institutions may look into new risk data sources in the next six months.

Appetites for new data ranged widely, but two distinct trends were apparent. Several participants mentioned that industry data would be valuable for assessing credit risk. One participant noted that “We will seek out additional industry data for at-risk borrowers”, whereas another noted that data covering which “Industries that will rebound or be resilient in [the] current environment” would be useful.

The other data trend? Real-time signals, or more timely data about how small businesses are faring given the impact of COVID-19. Participants repeatedly mentioned that more timely insight into a business’s revenue, cash flows, and other shorter-term signals would be valuable. One participant noted a need for “real time data rather than the typical bureau data that lags up to several months.”

Looking ahead

Our poll revealed that financial institutions are experiencing COVID-19 in diverse ways — and that they’re applying different strategies to resolving COVID-19 challenges. We’d love to know if the poll results resonated with you and reflected what you’re seeing at your own institution. Please reach out if you have feedback or additional insights to share.

By providing small business data that includes near real-time insights about small business credit risk as well as detailed industry data, Enigma is a resource at a time where better signal on small business risk and resiliency is urgently needed. If you’re interested in learning more about our small business data, feel free to get in touch or create your own account to explore our data right now.