Finding the Gems in Your Customer Base

The small and medium business (SMB) lending landscape is evolving rapidly. Existing institutional players like traditional banks and financial institutions (as well as the Small Business Administration) are increasing lending alongside new players entering the market. Amazon, which has been partnering with banks and fintechs since 2011, has lent close to a billion dollars to SMBs in the U.S.

This rapid acceleration and innovation mean SMB lending is growing more competitive for lenders, and those firms with established SMB portfolios have an advantage. Customers in the risk and underwriting spaces tell us it’s critical to find growing companies early and build relationships for long-term account value.

Risk and underwriting leaders: you’re uniquely positioned here. While you’re monitoring customer portfolios to mitigate risk, you’re also primed to spot opportunities: the growing “gems” in your customer base.

And to spot opportunity targets early, you need timely signals of growth.

We explored this challenge on a recent webinar. Charles Zhu, Vice President of Product, and Alexander Lee, Product Manager, unpacked:

- What revenue growth data is and how it can signal business growth

- Examples of promising businesses and their early growth signals, and

- How leaders can use this data to find customer gems.

Here’s an overview of their discussion.

Small business revenue data: See the trends, spot the needs

Chances are, you already have small business gems in your customer base with growth patterns that suggest they’re ready for new loans, credit line increases, or new products.

How can you offer your growing SMB customers additional access to the right kinds of capital at the right time, before your competitors?

Identifying growth trends early is key. Annual revenue numbers aren’t timely enough to be helpful here. But if you can get a look at a company’s monthly revenue, you can get a better sense of its health. Better small business intelligence means you could see:

- Seasonal peaks: When revenues repeatedly trend higher at designated points throughout the year, a working capital loan may help a business get through a busy season.

- Seasonal dips: When revenues predictably drop and bank statements show little cash on hand, a bridge loan might propel a business through an expected lull.

- Long-term growth: Businesses with revenues showing sustained growth promise to have varying capital needs throughout their customer lifecycle—gems to be prioritized.

Risk and underwriting leaders have a unique vantage point. While you’re monitoring portfolios for risk, with timely signals you can also watch for these early growth patterns within your customer base. But how do you introduce these signals of revenue growth?

Card transaction data is the key

One of the best ways to find revenue growth trends is by looking at card transaction data, generated whenever a credit card—whether debit, small business, corporate, or charge card, or even a “card not present” transaction—is used to purchase goods or services from a business.

The more society moves away from cash, the more powerful card transaction data becomes as a signal. A McKinsey study found that by the end of 2020, U.S. consumers used cash for just 28% of transactions, compared to 51% a decade prior.

Card transaction data is notoriously messy. But when it’s collected, cleaned up, and matched to businesses at scale, it builds a remarkably accurate profile of a business. More on this small business revenue data and how we aggregate it in our earlier post, “A Guide to Card Transaction Data.”

Card revenue data can offer other financial health insights, like transaction volumes, average transaction size, and ticket size. You can also get a sense of a business’s customer base, through customer transactions: is one whale spending $10,000 a month, or are 1,000 customers each spending $10 a month?

In combination, these attributes can paint a rich, meaningful portrait of a business. They can be used for signals of growth or signals of decline and risk. When we aggregate these different card transactions by business, we call it “merchant transaction data.”

In certain industries, merchant transaction data is especially strong: for example, restaurants and retail are almost entirely card-based, so this data becomes an accurate indicator of total revenue as well as revenue trend lines.

Real-life gems and hindsight

To see how this might play out with real businesses, we analyzed our data on a few companies from the headlines that have been on a growth path. We’ve overlaid key announcements onto the charts, like fundraising rounds.

With hindsight, we wanted to explore: what growth signals were present before the company’s success was broadly known?

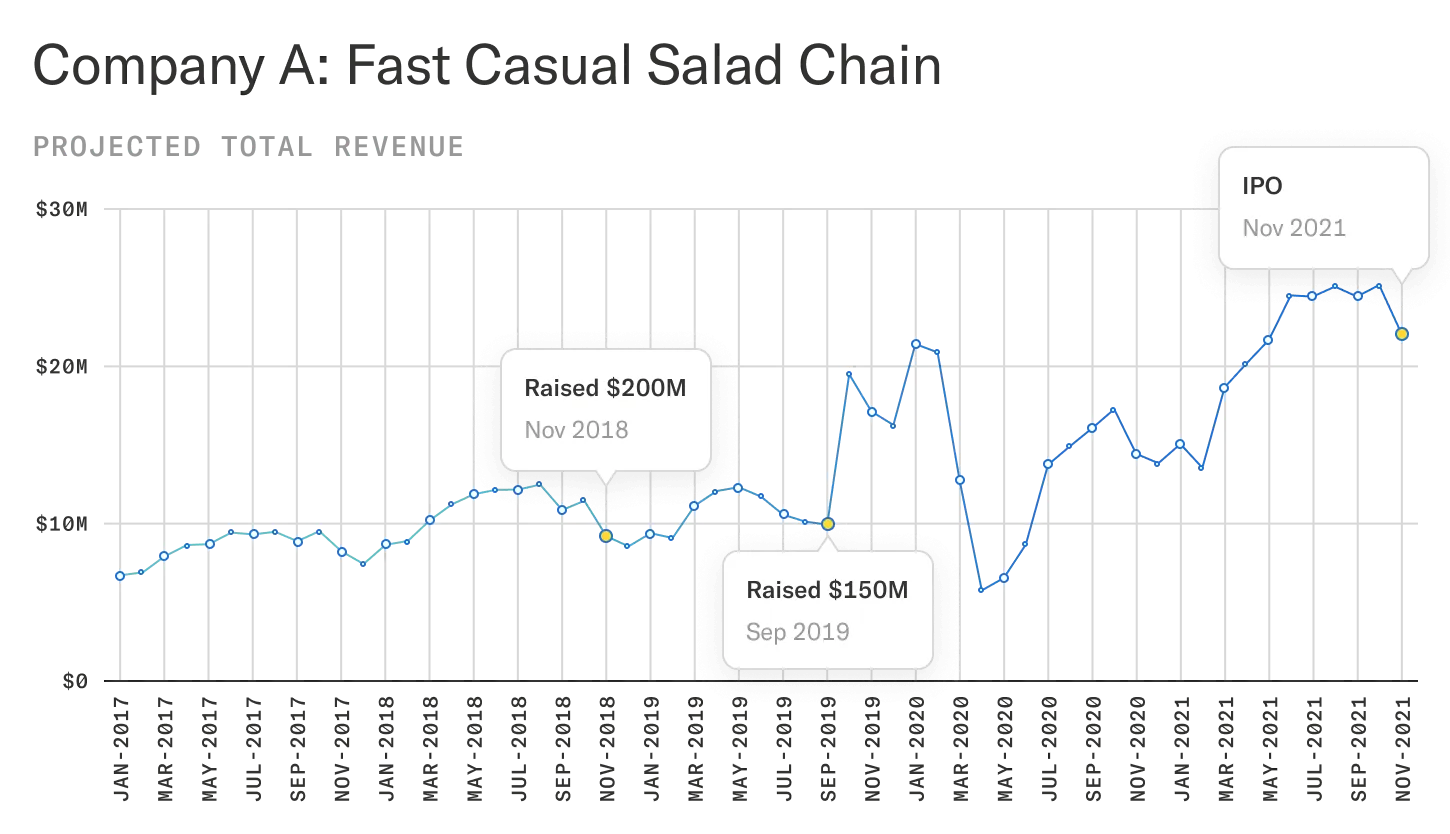

Company A is a fast casual salad chain established in 2007.

Long before its dramatic card revenue increases in 2019, we can see the company had about 50% year-over-year growth back in 2017 and 2018. Those growth signals would’ve shown up in the data before it was public knowledge that, say, the company was looking to open new store locations or secure the fundraising round it ultimately announced in November 2018.

We can also get a sense of performance through the pandemic. Revenues fell dramatically in early 2020 – then bounced back post-pandemic, leading up to the company’s IPO in November 2021.

We can see that card revenues for this salad chain tend to spike in the summer months compared to the winter months (prep for beach season?). Looking at card revenues at a granular, monthly level can help us understand seasonality trends for certain businesses and consider their growth needs through that lens.

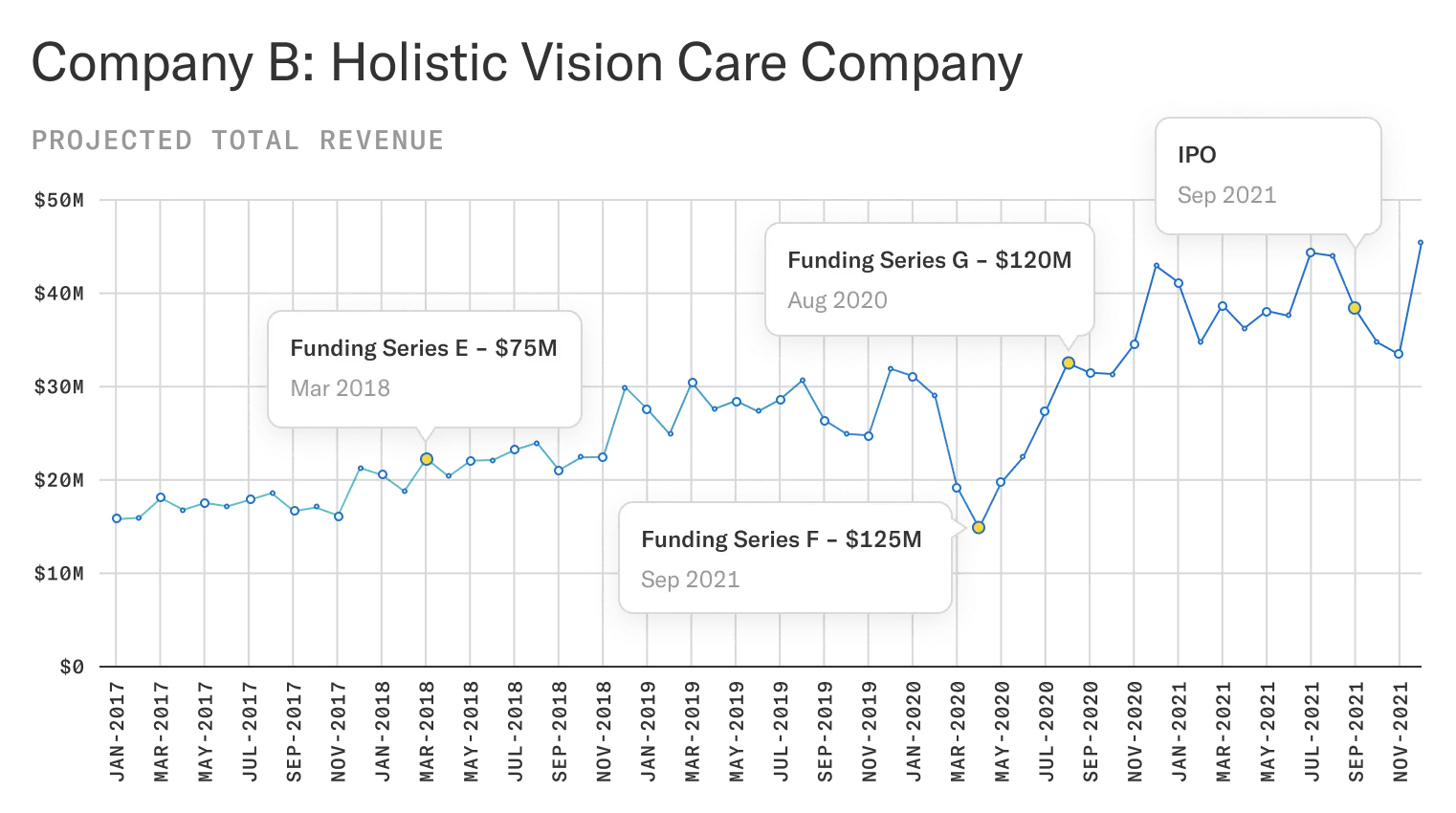

Company B started out as an affordable online shop for glasses and now offers a full range of vision care products and services, in-store and online.

Aside from a pandemic dip from April to August 2020, we can see the company’s card revenues have built steadily through its IPO in September 2021. We see modest revenue spikes each December, perhaps reflecting customers spending their use-it-or-lose-it vision benefits. During this timeframe, media coverage tells us that the company was steadily growing its brick-and-mortar footprint as it expanded products and services.

These examples may be larger companies than the small businesses in your portfolio. But they’re meant to illustrate how granular monthly revenue data can help you catch your customers’ signals of growth earlier — and respond proactively to better serve their evolving needs.

Small business intelligence for a changing landscape

As the small business lending landscape continues to evolve, organizations with existing SMB customer portfolios will have an advantage. The key is tapping into businesses’ growth signals so you can determine who’s ready for additional products and services — or will be soon. That’s a tough read from an annual revenue figure alone.

Card revenue data is a powerful tool for helping you to better understand SMB financial health and uncover the most promising businesses already on your books.

This article is based on an Enigma webinar. Watch the replay now.

Learn more: how a top-10 SMB lender found 70,000 gems in its customer base with Enigma data.